A plain‑language ELI5 guide to blockchain that explains how decentralized ledgers, nodes and miners create secure, immutable transaction records, how blocks and mining work, and where blockchain adds business value from payments to dApps and token fundraising.

- Decentralizes trust: Distributed nodes keep identical ledgers so no single middleman controls transactions, reducing fraud, censorship and single‑point failures.

- Economic security: Miners validate blocks through costly work; rewards align incentives and make tampering economically impractical.

- Business & investment potential: Practical uses include global payments, dApps (Ethereum), token fundraising (ICOs/STOs) and new market opportunities.

With all the buzz and hype around blockchain in 2026, it’s no surprise that you want to get in on the action.

This is why we created this all-in-one guide made so simple that we basically “explain it like you’re five” (ELI5 blockchain).

Throughout this introduction to blockchain guide, you will be unlocking the mysteries behind all of the blockchain basics – how Bitcoin works, what mining is, how a transaction works, and more.

So, sit tight, relax, and let’s start learning.

Note: this article is a simplified version of our guide “Blockchain for Dummies”

As you do your own research, you will commonly notice people using the words nodes and miners interchangeably. Miners aren’t normal nodes.

While banks are trustworthy for the most part, they can still freeze your funds, deny requests and have unreasonable fees.

Introduction to Blockchain: Your 2-Minute Review

Let’s begin your ELI5 blockchain guide with an analogy that will lay down the foundation.

Our example will take place in a historic city before banks existed. Members of the community barter for goods and make promises for loans, but after long periods of time, promises are broken and corruption rises.

Here’s how their issues are resolved better than banks, by using a decentralized , blockchain-like system.

A Simple Analogy: Block city, The Historic City

Let’s call this historic city Block City.

In Block City, people trade goods with one another – salt for sugar, milk for chickens, etc.

There are around 100 families that make up this city, and they place all of their trades through the city’s lead negotiator and middleman named Azarath.

Azarath coordinates deals, keeps track of promises (who is lending goods to whom), and keeps a fee for his work.

In many ways, Azarath is similar to a bank, acting as the middleman to facilitate transactions and is in charge of the city’s trade ledger.

Azarath was becoming extremely rich from being in his position, and greed began to take over.

Members of the city would actually pay Azarath big bribes to help them break promises (if they got a loan from fellow a community member) and pay him to update the ledger showing that payments were made, even if they weren’t.

Azarath continued to take these bribes and not only was his ledger filled with fraudulent transactions, but he began to lose track of the “real” status of outstanding promises.

The city’s ledger was becoming a mess and their economy was in danger.

Those who got cut out of deals began to point fingers at Azarath, calling him untrustworthy and corrupt. Block City agreed that a new system was required.

A fellow community member devised a plan to cut out Azarath as the central authority, and have everyone in the community manage their own, independent ledgers – where each ledger tracks all of the transactions in Block City.

Each week, the community planned to gather, confirm transactions, and update each other’s ledgers – forming a consensus.

This effectively decentralized the accounting system for the community, creating an environment where Azarath doesn’t need to be trusted as a central authority.

Let’s fast forward two weeks to their first meeting. The 100 families gathered one evening and all presented their ledgers to one another.

Since everyone’s ledger showed outstanding debt, all transactions were confirmed and all debts that were owed were paid.

Once debts were paid and any mismatched ledgers were settled, then all of the community members would update their ledgers together and be in agreeance.

If there were a few evil members of the community trying to be corrupt, it would show in their ledger. A majority of the community would disagree after checking their ledgers, and the evil members would create a bad reputation for themselves.

Instead of trusting one person, now every resident of Block City needs to trust that the majority of the community will act in a trustworthy manner.

As long as this system works, then there are no worries. This is where blockchain technology jumps in; it automates trust amongst the community, creating a trustless environment.

To reiterate once more, this concept of decentralization, where everyone has their own ledger of transactions, is precisely how the blockchain works at a technical level.

Okay, enough analogies, let’s dive into how this stuff really works.

ELI5 Blockchain: How It Works (in a nutshell)

Now that you understand that the blockchain is a distributed ledger and has a well-defined process that validates the updates, let’s understand the process and components that really make it up.

Although we are moving forward, we are still keeping this ELI5 blockchain guide as simple as possible.

Next, we will gain an understanding of:

- Decentralization and nodes …what the heck does this mean?

- What is a block ? What is the chain?

- How does a transaction work?

- What is mining ?

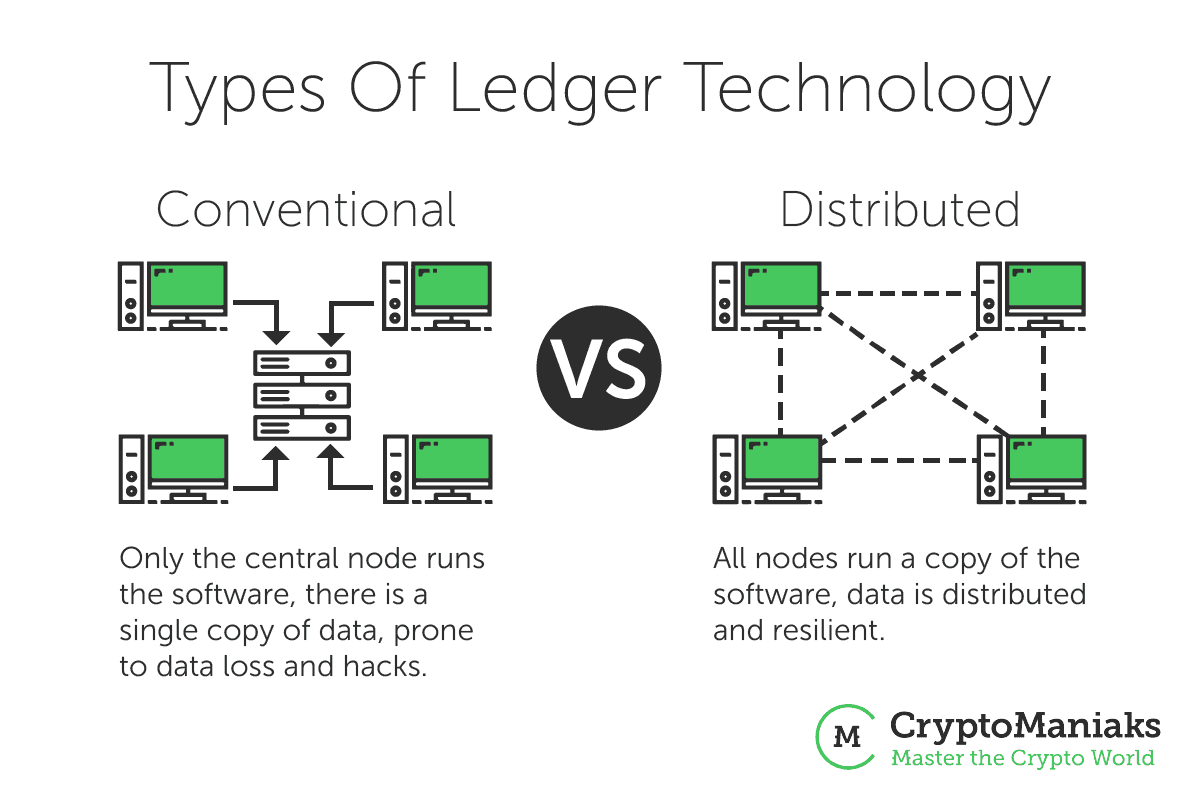

Decentralization and Nodes – What Does It All Mean?

In our Block City example, we mentioned that a community is made up of individuals who must keep their own individual ledgers.

This is analogous to each community member acting as a node .

These nodes have their own versions of the Bitcoin ledger, just like Block City members managing their individual ledgers.

In Bitcoin’s case, a node is someone who downloaded Bitcoin’s blockchain and is helping to verify transactions to keep the network accurate and moving.

There are different types of nodes that do more or less work, but for simplicity’s sake, just understand that a node is anyone who downloads the Bitcoin software and is helping to keep the network alive.

As you do your own research, you will commonly notice people using the words nodes and miners interchangeably, but we want to be explicit that miners are not normal nodes.

Miners must download special mining software and their purpose is to not only verify transactions like nodes, but also grab transaction requests and actually create new blocks that all nodes must update their ledger’s with.

Without miners, the blockchain would be frozen and transactions wouldn’t move. It’s as if no bank employees were at work to transfer funds for you.

What is a Block? What is the Chain?

A block records some of the most recent transactions that occurred in the network.

In the case of Bitcoin, a block has the most recent transactions within the past 10 minutes.

Bitcoin has a block time of 10 minutes, which means a new block is created and added to the blockchain every 10 minutes.

The chain is the global, completely historic list of all blocks, and thus, a complete record of transactions that have ever occurred.

Each block is mathematically (cryptographically) linked to the block before it.

Put simply, each block has a reference to the block before it, so the database cannot be tampered with, and becomes immutable as a result.

As you can imagine, downloading Bitcoin’s blockchain can take a while. It is 100s of GBs large – not your typical text document.

This is a large piece of software that only dedicated nodes and miners download, you as a user do not need to download the blockchain ledger.

What is Mining?

Let’s move forward with our ELI5 blockchain guide by explaining how mining works.

Mining is the process of grabbing transaction requests and adding them to the next block. Miners are then rewarded for their work through block rewards .

All of this is automated, it is not a computer game where you sit there and mine. Simply download the mining software and let the computer work for you.

Mining is generally explained as a game, where the first person to figure out the answer to the next block of the blockchain receives the block reward, inherent in blockchain software.

In Bitcoin’s case, the block time is 10 minutes, which means every 10 minutes successful miners receive Bitcoin through the block reward.

The first miner(s) to solve the ‘answer’ to the next block wins the block reward.

Moving forward with our introduction to blockchain guide, we will explain the literal steps in the mining process by walking you through a transaction in action.

A Transaction in Action

You send your friend Bob 1 Bitcoin. A few minutes later your friend Bob received the 1 Bitcoin in his wallet. How?

Let’s break this down step by step, and explain the role of miners since it is integral to the process:

- You send Bob 1 Bitcoin and sign the request with your private key . Upon doing this, your transaction request (sending Bob 1 Bitcoin) is broadcasted to the global, decentralized Bitcoin network. At this point, Bob has not received your Bitcoin yet, your transaction is in limbo, waiting to be confirmed and added to a block.

- Miners grab your transaction along with several others and individually race to solve the answer for the reference of the next block. So, the miners grab transactions, turn their backs and privately mine away at this math problem.

- A miner solved the problem, turns around and faces the network to broadcast their new version of the blockchain which includes your transaction.

- Other nodes and miners in the network agree that all of the transactions in the miner’s proposal are valid, then the miner(s) who proposed the new valid block will receive Bitcoin as a reward. Additionally, Bob will receive your 1 Bitcoin since it is now part of the blockchain ledger.

- At this point, the mining process starts over again. Inevitably there are more transaction requests broadcasted to the network. Miners grab them, turn their backs, mine, propose an updated version of the ledger and so on.

Without miners your transaction would have never been received by Bob, it would be sitting in limbo forever.

This is why miners play such an important role.

Why Blockchain is Secure

The big reason blockchain has gained traction is not obvious at first, but relax and we’ll explain this blockchain topic like you’re five.

Banks have become corrupt, many government-backed (fiat ) currencies are no longer based on the gold standard, and people no longer control their own money – it is owned by banks.

While banks are trustworthy for the most part, they can still freeze your funds, deny requests and charge unreasonable fees.

Until blockchain technology, we have needed banks to act as trusted third parties. But banks are no longer needed.

Let’s see why.

In a nutshell, financial incentives make the blockchain secure. Since miners are rewarded in cryptocurrency, and invest $1,000s in mining hardware, then there is a financial incentive for nodes to act honestly.

If they act maliciously, then their work will be rejected by the network, wasting computing time and the value of their mining hardware.

Ultimately, Blockchain technology and the mechanisms that come along with it (miners, nodes, checks and balances), offers a trusted decentralized network controlled by no one individual.

It allows individuals to transact globally, without a middleman. This is just a glimpse into some reasons why people love blockchain.

It brings trust to peer to peer networks, which has never been seen before – let’s explore more.

Who Invented the Blockchain?

You may be wondering who invented the blockchain; it’s a funny story.

The funny part here is that no one knows for certain who invented blockchain, and Bitcoin which came along with it.

The inventor goes by the name Satoshi Nakamoto and it may represent one person or a group of people.

There are theories on who it is, but no one knows for certain.

The white paper was released anonymously, and “Satoshi” currently has 1,000,000 Bitcoin in his wallet, according to Bitcoin’s blockchain ledger.

Scroll to the bottom of this page to see the first-ever 50 Bitcoin minted into existence!

Blockchain Applications to the Real World

Now it’s time to get practical. This wouldn’t be an ELI5 blockchain guide if you walked away with no clue of any real-world uses.

Investors are pouring money into blockchain-related startups because real-world applications are evident.

Many compare the blockchain revolution to the internet in the 90s – people are just starting to see its potential.

Some real-world use-cases are that it:

- Gives people power over their own finances

- Improves many industries other than only financial ones

- Is accessible to low-income nations and creates marketplaces for everyone

Giving Power Back to the People

As mentioned, banks freeze user accounts, they charge high fees due to inefficient operations, and they also can get hacked.

Blockchain technology ultimately offers a trustless environment for peer to peer transactions, which means no one has to trust anyone except the technology itself.

In the end, people have control of their own money.

You keep your Bitcoin on your computer and can send it any time of the week and any time of the day, to anywhere in the world with negligible fees, all completed nearly instantaneously.

This technology has never been seen before – it can take days or weeks using regular financial services to send money internationally due to the bureaucracy behind banks.

Giving Power Back to Businesses

These decentralized blockchain based networks offer small and mid-level companies the opportunity to house their data on these networks, allowing these companies to save money on server costs.

Additionally, there are now new ways for businesses to raise funds, by taking advantage of the ICO industry (initial coin offering).

An ICO is when a business issues its own cryptocurrency and sells it to investors to raise funds.

If the token is useful and the company is a success, then ICO investors can expect to make money off of the token, similar to buying shares (but not equivalent!) in a company.

ICOs are mostly hosted on a platform called Ethereum, which we will get into next.

Distributed Applications (Web 3.0)

One blockchain project in particular that has gained traction, almost as much as Bitcoin – is Ethereum .

Unlike Bitcoin which has a focus on monetary transactions, Ethereum is a platform which allows developers to create applications and launch them on Ethereum’s decentralized, global ledger.

These applications are called decentralized, or distributed applications (dApps ).

Ultimately, this can turn into a new internet, known as the web 3.0.

Ethereum in Action

As mentioned, Ethereum is a dApp platform. It has its own programming language, Solidity , and developers can launch their own applications.

One great business advantage is that, unlike apps, dApps, can be used globally by anyone.

This means the dApps creators can hit a larger user base, globalize advertising, and ultimately, increase revenue.

Cryptokitties is one great example of a fun, viral Ethereum based dApp.

The Future is Bright

Despite market cycles, Bitcoin and cryptocurrencies have value and the future is bright for the cryptocurrency market.

Blockchain technology will continue to mature and new trends will emerge.

There was the ICO boom in 2017, next people anticipate STOs (security token offerings) for public companies.

Wallets and services around cryptocurrencies will continue to become more user-friendly for people of all ages.

The goal is to get cryptocurrencies into the hands of everyone around the world. It’s worth getting in before it goes mainstream.

I Want in on the Blockchain Revolution

Glad to hear!

This introduction to blockchain was just a taste providing you with the basics.

If you are intrigued, we recommend getting involved now.

If you can get in before Wall Street and institutional investors then you will likely see some profits in your future.

The market cap of Bitcoin is nowhere near gold, which means it has the potential to grow another 100x.

To begin investing in cryptocurrencies, check out our free online course.

On the other hand, if you’re more interested in the technology and would like to get involved in development, then check out our friend’s course over at Blockgeeks.com for some hands-on experience.

We're sorry you did not find what you were looking for. Please select the reason this article was not helpful.