A concise 2025 primer that explains blockchain basics—how blocks, nodes, miners and consensus work—plus why decentralization, immutability and wallets matter for security, costs and real-world applications.

- Disintermediates trust: Blockchain removes middlemen, slashes fees and enables direct peer-to-peer value and data exchange across industries.

- Security & mechanics: Distributed, immutable ledgers secured by cryptography, nodes and consensus (e.g., PoW) grow more robust as networks scale.

- Broad strategic impact: Use cases span banking, supply chains, voting and storage; large tech and enterprises are investing, so foundational knowledge has clear business value.

Blockchain was introduced as the underlying technology that powered Bitcoin – the first cryptocurrency.

Think of it as the infrastructure for cryptocurrency – if cryptocurrencies were cars, blockchain would be the roads.

Although there’s some debate amongst experts about the future of cryptocurrencies, there’s no debate about the bright future of blockchain technology.

In this 2026 blockchain for dummies guide, we will make sure blockchain is explained in simple terms.

Blockchain Is The Next Big Thing

Everyone agrees that the tech is a huge advancement – probably the biggest since the dawn of the internet.

As a result, most big companies like Google and Amazon are fighting to get their piece of the cake by working on their own blockchain solutions.

Putting in the time to read this blockchain 101 guide will pay off tremendously.

Compare this to reading a book about the internet back in 1994, when TV shows were still discussing the birth of emails.

The future of decentralized technology is bright, and whether you’re interested in cryptocurrencies or in blockchain technology, knowing the basics of blockchain is a must.

This includes a simple explanation on how do blockchains work, what problems they solve, and their incredible benefits to the world.

Curious about cryptocurrencies and not so much the underlying tech? You might have missed our introductory guide on Bitcoin, check it out!

What This Blockchain for Dummies Guide is NOT About

We want to make it clear that this blockchain for dummies guide will not be about learning how to develop blockchains or anything technically advanced.

If you are thinking of becoming a Blockchain professional, or if you want to learn more about its technical aspects, we suggest you check out our partner Blockgeeks (use our exclusive coupon codes CryptoManiaksPRO and CryptoManiaksACC for 20% discounts on their premium products).

They offer the best resources available online for this purpose and have already trained an incredible number of blockchain professionals.

Blockchain technology is changing the world around us and we’ll cover many of its applications within this blockchain 101 guide.

Let’s get started!

Blockchain For Dummies: A Simple Explanation

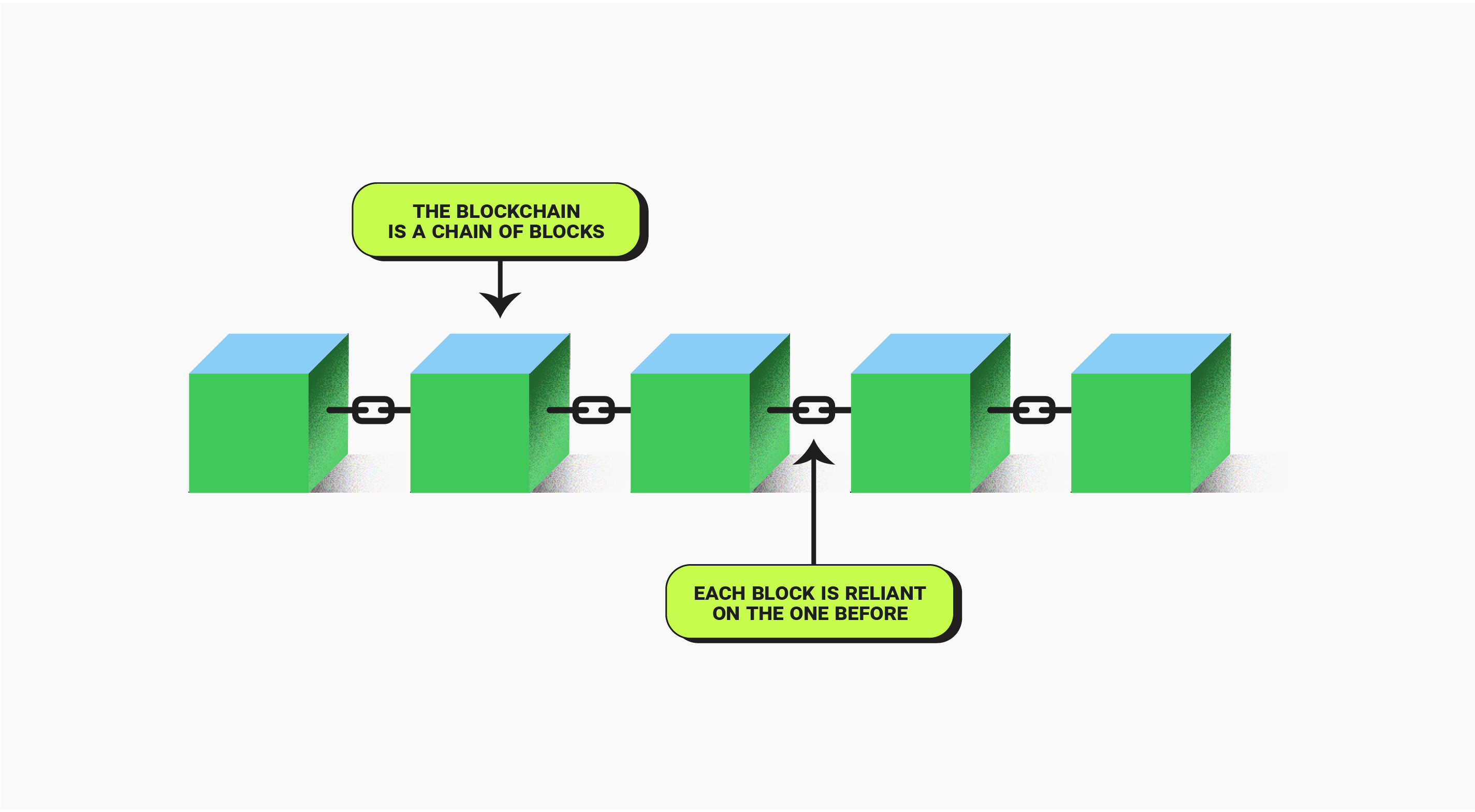

A blockchain is basically a chain of blocks . Blocks contain digital information – picture them as packets of data all tied up, like a Christmas present.

In the case of Bitcoin’s blockchain:

- Inside each block is a series of Bitcoin transactions that have taken place within a certain timeframe.

- All the blocks together constitute Bitcoin’s blockchain and witness all the transactions that occurred since its creation.

What was the First Platform That Used a Blockchain?

Bitcoin, the first working example of blockchain technology, was invented as a response to the inefficiencies of centralized banking institutions.

Its launch in 2009 immediately following the 2007/2008 financial collapse is not a coincidence.

The creator(s) of Bitcoin were inspired by democratic idealism encouraging individual autonomy within the monetary system.

Where is a blockchain located?

By essence, blockchain is a network of computers that can be located all over the world.

Computers contributing to a given blockchain possesses the data or transactions that have ever been written on that blockchain.

This specific characteristic is what makes blockchains decentralized and incredibly robust, as they are able to survive power outages and political turmoil.

The more computers the stronger the blockchain. This is how blockchains work in a decentralized manner.

Is There More Than One Type of Blockchain?

There are probably over 10,000 blockchains in existence today. Most blockchains are either public or private.

Public Blockchains. In this example, an open source software is used by everyone participating in the network. Anyone can join and the network has a global foundation. For example, a lot of cryptocurrencies are built on existing blockchains, ERC20 tokens being the most well-known example built on Ethereum .

Private Blockchains. These use the same principles as public ones except the software is proprietary and hosted on private servers instead. Companies such as WalMart are developing their own blockchains to track supply-chain logistics.

Technical Benefits of Blockchain: An Overview

Blockchain technology is one of the most promising new technologies to date.

It provides a method of recording and transferring data in a transparent, trusted, and provable way.

It allows individuals and companies to engage in a transfer system that is fully transparent, democratic, and secure.

Most importantly, it allows trust-less storage and transactions, removing the need for intermediaries. You might not realize the impact of those benefits yet, so here are some examples to help you.

- Visa monetizes trust as the intermediary between merchants and customers.

- Amazon monetizes trust as the intermediary between sellers and customers.

- Uber monetizes trust as the intermediary between drivers and customers.

And the list goes on. If you notice, every single example requires trusting an intermediary with your information.

Having a central point of data collection poses a security risk, your information no longer belongs to you, a company now owns it. What they do with it is their prerogative.

The adoption of blockchain technology will remove the need for third parties and will allow trust-less peer-to-peer transactions.

In the worst-case scenario, it will reduce the costs for companies and the fees for the end-users of a trust-based service.

In the best scenario, it will completely remove the need for intermediaries in most industries.

Practical Benefits of Blockchain: An Overview

The blockchain is already disrupting industries such as:

- Banking and Payments. Blockchain technology can give financial services access to the “unbanked ” of the world. It will make the monetary system more transparent for the “banked” people as well.

Most banks are also developing their own blockchain solutions as it will make their operations faster, more secure and efficient. - Online Data Storage. Cloud storage systems, as we currently know them, rely on large centralized databases. This leaves data vulnerable to privacy breaches and the potential for environmental catastrophe. Blockchain makes data safer by removing failure points. It will also create even more cost-effective storage options.

- Voting. Blockchain will make elections more transparent and fair than ever before in the history of humanity.

Blockchain technology is currently disrupting, or it will disrupt any industry that involves data and transactions.

This includes economic sectors involving intermediaries that monetizes trust, think bureaucracy in financial companies and even the governments.

From here, our blockchain for dummies guide will dive into each of the aspects we just touched upon more in-depth. From the benefits of the blockchain to the problems it solves, including some more advanced concepts.

If you don’t really care about the technicalities of blockchain and its interaction with cryptocurrencies, skip and read the chapters relating to the benefits of Blockchain Technology.

How Do Blockchains Work

Introducing Miners

The term “miner ” is ever-evolving and each blockchain has unique specifications for the word.

To keep it simple, we are going to refer to miners as individuals or companies running special software to build onto the Bitcoin blockchain.

Miners are essential to make the blockchain operational, without them, there would be no computers running the network and no way to conduct transactions with it.

To incentivize miners, rewards are usually given to the computer which finds the next block in a public and open-source chain, like Bitcoin’s blockchain. The rewards are generally distributed through cryptocurrencies.

Where is the Blockchain Stored? Let’s talk about Nodes

Nodes refer to computers hosting a copy of the blockchain.

Unlike miners, they are not incentivized to find the next block in the sequence, instead, they validate the transactions and communicate with other nodes and miners.

You can think of nodes like relay towers, helping the underlying blockchain update itself and stay accurate.

How Are New Blocks Built and Validated?

Each block within a blockchain holds some data. In the case of Bitcoin, data is a series of transactions. That data is organized in a single digital folder.

This folder – the block in this case – is confirmed by a miner, who adds it to the previous block in the blockchain.

New blocks of transactions are written into Bitcoin’s blockchain every few minutes. This is called “mining ” blocks. This action links the new blocks to the already existing chain of blocks.

But in order to be added to the existing chain of blocks, new blocks need to be validated.

This is the role of nodes. In the case of Bitcoin, nodes are in charge of validating Bitcoin transactions that occur across Bitcoin’s network.

The way this works is that miners choose which transactions to include in a new block.

Next, nodes verify all the transactions in the block. Lastly, if everything is good, nodes relay the new block to other nodes.

The Protocol Dictates the Rules of the Blockchain

Every blockchain is based upon a protocol (or “consensus algorithm”). A protocol is an agreed-upon method of interaction between computers. You can think of this like the rules each machine within the network must follow.

For example, Bitcoin has some specific rules which keep the protocol standard across all machines:

- 1 block is added every 10 minutes. This usually depends on each blockchain.

- The amount of Bitcoin given as a reward to miners reduces every 210,000 blocks. This translates into Bitcoin having a finite supply, 21 million in total.

- Miners must solve a complex mathematical problem in order to find the next block. The protocol ensures the difficulty of finding the next block increases or decreases in relation to the number of miners competing against one another.

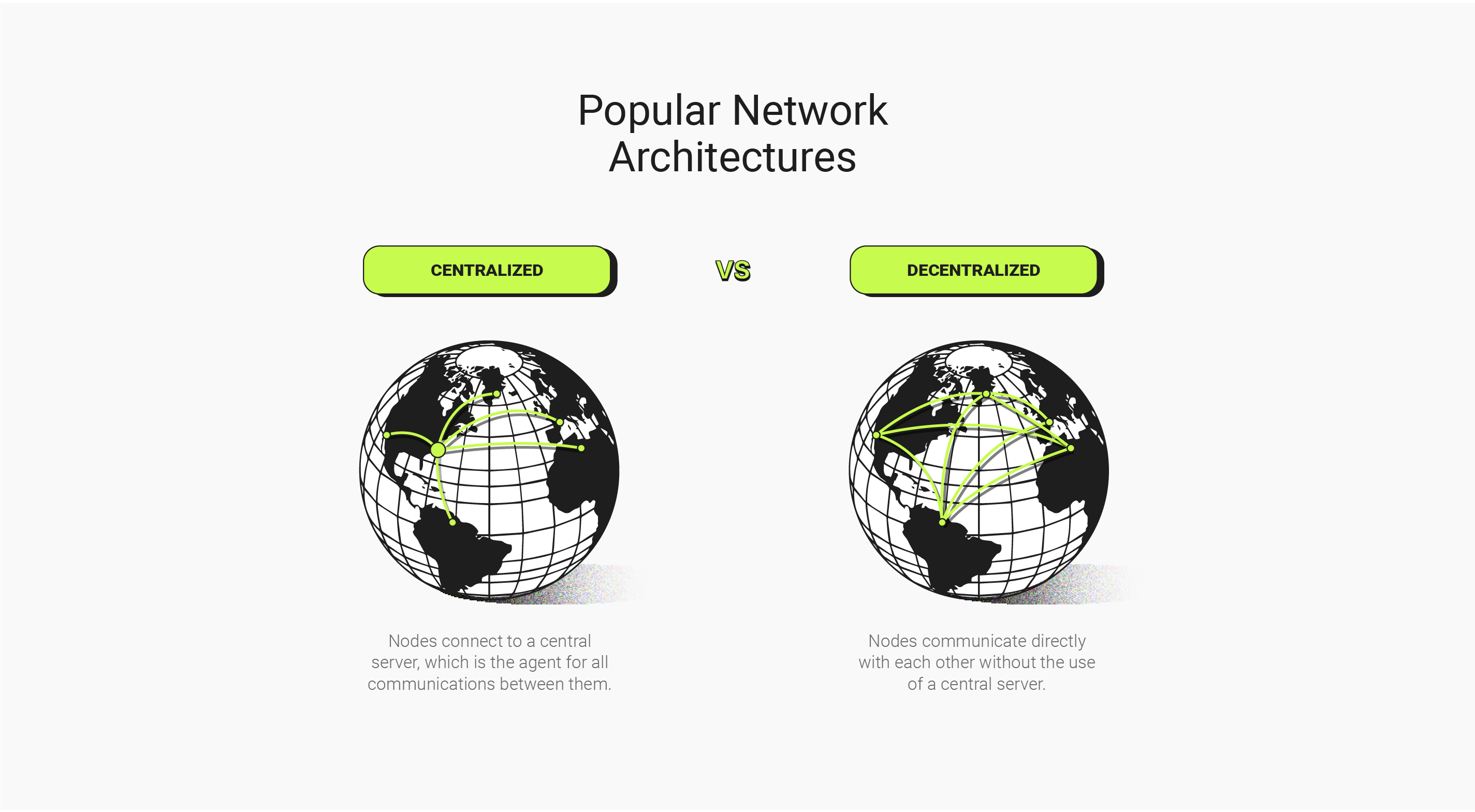

Blockchain Is Decentralized. Why is it Important?

The blockchain’s software is run by individual computers connected to each other via the internet from all over the world.

Each computer in a blockchain is running the same software. If one is disconnected, the network stays operational.

Even if every computer in the world shuts down simultaneously, the blockchain is still storing its data in distributed ledgers.

If all of the world’s power goes out, computers will have a copy of the ledger from when it was last updated. We wouldn’t be able to update the ledger until power was restored but BTC won’t disappear.

This characteristic makes the technology incredibly robust, able to survive power outages and political turmoil.

The blockchain is a method of trustless digital exchange, spread across multiple machines, all running the same program.

By distributing ledgers across every computer running the protocol, blockchains remove the need for the middlemen, centralized authorities and third parties.

Without third parties, users can interact with each other directly without needing to trust or compensate any centralized corporations or governments to do business.

It’s a form of Peer-to-peer (P2P) collaboration.

This in itself is not a new or a radical idea; Services like Napster and Limewire enabled the same principle in the early 2000s.

The difference lies in the ability to store digital information – including transactions – in a distributed ledger that promises immutability .

How is the information maintained: Distributed Ledger Technology

In order to maintain transaction history over time, copies of all the blocks are distributed amongst the participants of a blockchain.

These participants are called nodes. Miners build the blockchain by mining blocks, but anyone can act as a node.

Nodes run the blockchain’s software and continually update themselves with the most recent blockchain information.

There are different types of nodes:

- Full Nodes

These computers run a full copy of the blockchain which contains information dating back to the genesis block . - Lightweight Nodes

Running this version only contains information dating back a few weeks, or maybe even a few hours. It’s faster to run on a machine but has the possibility of not being as accurate or secure because you’ll have to trust others to provide the data you are missing.

Hosting a node helps keep the blockchain updated and accurate.

Nodes and miners are constantly cross-referencing each other in order to build and maintain the blockchain.

When information is kept on multiple machines it is known as Distributed Ledger Technolgy, or DLT. Blockchain is one of the most well-known examples of this technology.

Banks Host a Centralized Ledger

A good example of a real-world situation is your bank. In order to record all the money being deposited and withdrawn, the institution itself keeps a centralized ledger.

You are paying them for this service, it’s one of the major reasons banks were invented. It’s also a costly investment which requires physical infrastructure and professionals working around the clock to keep it operational.

The decentralized way in how blockchain works is in contrast with traditional banks.

The blockchain is hosted by everyone in the system, foregoing the need for an expensive headquarters. Compared to a centralized system, it has no weak points and it’s more cost effective.

The Bigger the Better

Recall the previous chapters of this blockchain for dummies guide.

Did we mention the importance of miners? Yes, we did. But we didn’t explain it into much detail.

Miners use CPU power and electricity to validate the next block in the Bitcoin blockchain.

Using primary resources such as electricity and computing power to validate blocks is called Proof-of-Work.

This real-world cost is what makes the Bitcoin protocol so robust. Every block within the chain is unique – think of it as a tangible digital asset.

The more miners hosting a network, the stronger it is.

Compare Bitcoin, which has the largest miner network of any cryptocurrency, to a brand-new blockchain that’s just being launched.

This new protocol has fewer miners, which translates into greater centralization, more weak points, and less primary resources building and protecting information.

The longer the blockchain becomes, the stronger it becomes.

Bitcoin’s blockchain is so huge that it would take more computation power than currently exists to try and recreate it.

This makes transactions extremely trustworthy and the protocol extraordinarily strong.

Applications to Cryptocurrencies

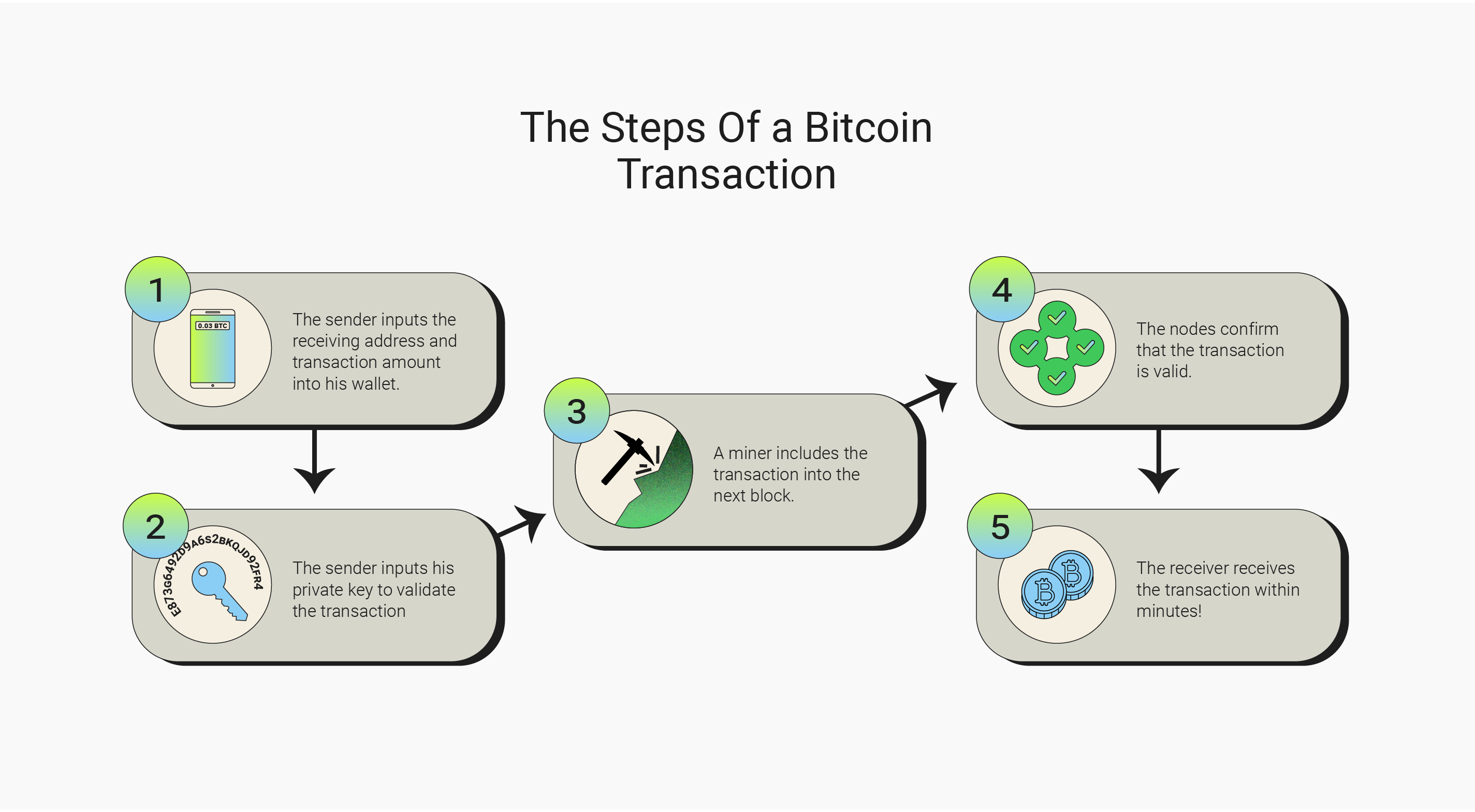

An Example of The Bitcoin Network In Action

This is a very basic example of how a Bitcoin transaction works. It outlines the basics and should help you begin a journey into the wonderful world of cryptocurrency.

- Paul wants to send 0.01 Bitcoin from his wallet to Ashley’s.

- Opening his wallet, he inputs Ashley’s public address into the “send address” field.

- To confirm the transaction output, Paul enters his private key into his wallet which confirms the amount and sends the transaction to the blockchain.

- Doug – a miner – charges 0.000056 BTC. The fee acts as an incentive to the miner to include the transaction into the next block within the blockchain. Paul’s wallet will automatically add the fee to the transaction’s total amount.

- Nodes confirm that the transaction is valid and add it to their own version of the blockchain.

- Ashley’s wallet receives the transaction within minutes.

Transactions are time-stamped and added to a block every few minutes. In the Bitcoin protocol, the time between blocks is roughly 10 minutes.

Proof of Work is a foundation to Bitcoin’s value

Consensus algorithms take the place of trusted third parties in peer-to-peer networks.

Now, there’s no need to trust a bank or a centralized escrow. Instead, we can trust a decentralized system of individual nodes that come to an agreement.

Proof of Work is the consensus algorithm that was made famous by Bitcoin. Proof of Work is accomplished with hardware. Miners use mining rigs that continually attempt to find the next block of Bitcoin’s blockchain.

Basically, mining is like solving a difficult math problem through guessing.

The more guesses per second one can spit out, the better chances they have of finding the right answer first.

The person (or group of people) that finds the next block first receives a block reward.

This is how blockchain transaction validation is completed in PoW schemes. Miners and nodes validate newly proposed blocks. People invest anywhere from hundreds to millions of dollars in mining equipment (generally GPU’s, fans, and lots of electricity).

PoW is what makes Bitcoin the most robust and trustworthy cryptocurrency in existence.

As more miners compete to add blocks, the difficulty of solving the encryption increases. More CPU power is required and more electricity – both of which have real-world costs.

It’s this underlying infrastructure that makes the Bitcoin so secure and stable in comparison to other cryptocurrencies.

How do Bitcoin Wallets and Addresses really work?

Users of the Bitcoin network are able to transfer BTC to anyone in the world.

To do so, participants use a piece of software known as a wallet. Anyone can generate as many addresses as they like, no personal information is required to do so.

Once created, each wallet generates a public address and a private key. Each has a different function and understanding how they work is essential when navigating the cryptocurrency space.

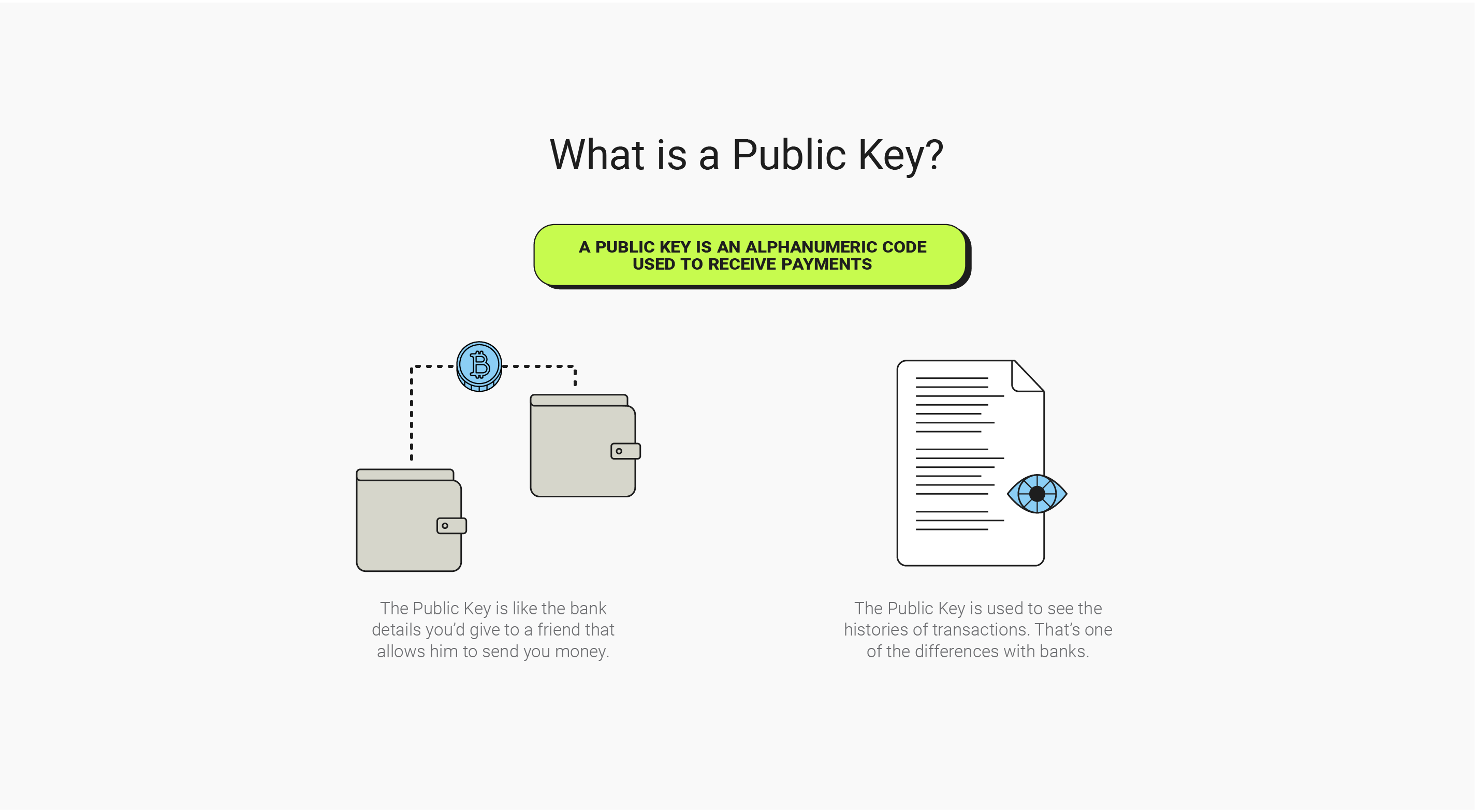

What is a Public Key?

A Public Address is an alphanumeric code, a unique identifier that links transactions with the sender and receiver.

For example 3D2oetdNuZUqQHPJmcMDDHYoqkyNVsFk9r – which is currently one of the richest Bitcoin addresses.

The public address is used to:

- Receive payments. Think of it like the bank details you’d give to a friend that allows them to send you money. If you want to receive Bitcoin from friends, create a Bitcoin wallet and send them your public key.

- Access the transaction’s history in relation to this public address. This is one feature that makes Bitcoin pseudonymous : The transaction’s record is public and accessible by anyone thanks to the public key of a wallet, but nobody can know who owns the private key that allows access to the funds.

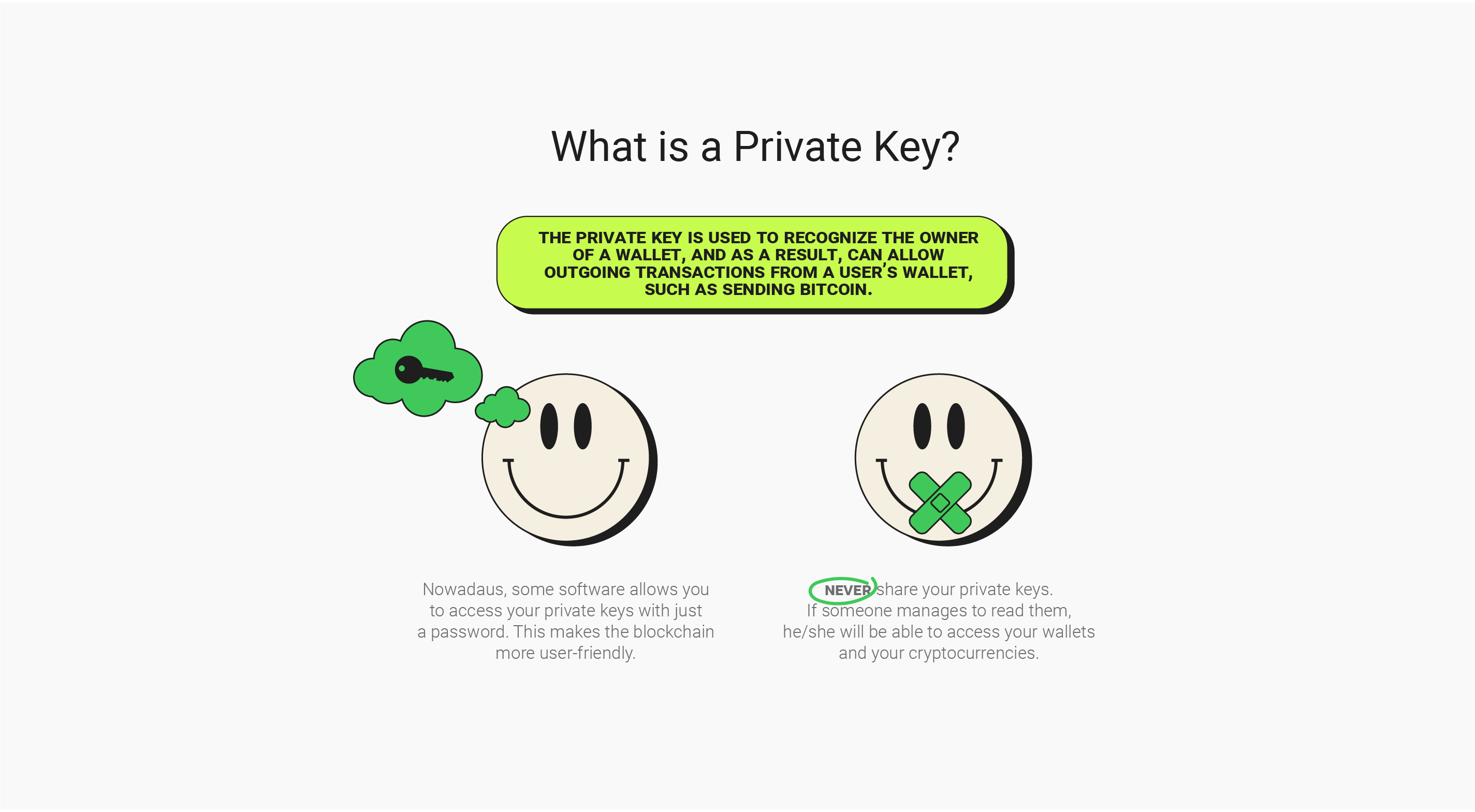

What is a Private Key?

The Private Key is very different, and you need to be sure to understand the difference.

A private key is also an alphanumeric code, but this one gives access to the funds of a wallet.

It allows someone to execute transactions from a wallet, like sending Bitcoin to another wallet.

Without the private key, it is impossible to access funds sent to a public wallet address.

The private key is only generated once and it is imperative to protect it at all costs. If it’s lost, there is no way to access your funds. There is no program that can retrieve a lost key.

You should never communicate your private key with anyone.

Benefits of Blockchain Technology

The Value of Blockchain Technology

The primary value of blockchains is the ability to store, verify, distribute, and permanently record large amounts of data, including transactions records, allowing the removal of a trusted 3rd party.

The technology automates information exchange across all digital mediums. A revolution is coming, led by blockchain technology.

Blockchains allows immutable data

All information stored on the blockchain is permanent and unable to be changed – immutable .

Compare this to traditional storage methods that require a 3rd party.

The requirement of human involvement for trusted transactions inevitably leads to corruption, bloat, and inefficiency.

Blockchain has the ability to automate every single one of these aspects potentially causing massive fiscal and social change.

Bitcoin proves blockchain is capable of operating and acting as the underlying infrastructure for a new monetary system.

Its immutability is also useful for hosting videos and streaming content.

With blockchain, users can create unique content that cannot be stolen and duplicated infinitely, allowing them to better monetize their work.

Blockchains are not controlled by any single entity.

Google, Facebook, Amazon, and Microsoft, these companies control the internet. The majority of emails, pictures, videos, and information shared online is stored on their proprietary servers.

Their services aren’t free, you are the product. When you use a “free” internet service, like Gmail, the company is monetizing your information, collecting your personal habits and selling that information to the highest bidder.

The dominance of a small number of companies on the internet is a phenomenon known as centralization and it leads to corruption and reduced incentive for technological advances.

Blockchain Creates Digital Freedom

In contrast to our current tech space, public blockchains and the cryptocurrencies built on them are decentralized. There is no organized company or group of people controlling the information stored on them or even how they operate.

Blockchain technology is going to challenge current monopolies in the tech space.

The world is now accustomed to sharing digital information and monetary transactions via the internet.

Blockchain technology further improves upon our technological experience and creates an infinite number of possibilities for people to engage with each other without relying on companies and 3rd parties.

It’s bringing freedom and entrepreneurism to the digital world on an individual level.

Blockchains have no single point of failure, which improves security

Current tech companies are plagued by hacking attacks where nefarious actors access and steal private information.

It has gotten to the point that your email address and even credit card information has been sold or stolen at least once.

There are industries built around the collection of valuable information. You can find out if you have been compromised in a data breach here.

Centralized systems are inherently at a disadvantage because criminals know where their information is kept. Decentralized systems, on the other hand, do not have a weak point.

Large public blockchains are distributed across hundreds of thousands of computers, it would be impossible to attack every single one simultaneously. This makes blockchain incredibly robust and secure.

Let’s say you are buying a pair of shoes online. These aren’t mass-produced shoes you find on Amazon, these are handmade, and they look amazing.

The artisan with whom you want to conduct business has a small operation and they rent space on a server to host their website. They use a simple plugin to help with credit card transactions.

Unfortunately, without their knowledge or yours, the server where their website is stored has just been compromised and all of your private data has been collected by a malware.

If instead, the shoe-maker opted to put their Bitcoin public address on their website, you could have ordered a pair of shoes and sent them Bitcoin. This way, his private key is not going to be compromised.

If you use a traditional bank, for example, you’re placing tremendous trust in that bank. You’re relying on them to handle your money safely and you can only hope that they provide the services they promise.

Many times, reality doesn’t match these expectations. Individuals experience delays in payment, withdrawal, and money transfers.

Every day, accounts are frozen or limited for reasons that customers do not understand.

Banks can even go bankrupt – like the Lehman Brothers.

Automation of Value Exchanges

Blockchain automates exchanges of information (including transactions). Instead of trusting a company, users trust a computer program with preset rules.

This reduces fees infinitesimally. For example, users can transfer millions of dollars worth on blockchain networks for less than $1.00.

As the competition in digital transactions heats up in the blockchain space, lower cost and faster options will continually be invented.

The days of paying credit card companies fees and relying on Paypal for online purchases are coming to an end.

Reduced Fees for Merchants and Consumers

Miners building the network and confirming transactions do charge a fee.

Each one is competing with other miners to solve the cryptographic puzzle and have the chance to build the next block. This keeps costs proportionally low.

The automation of the transactions also reduces corporate bureaucracy. If you don’t need to pay thousands of employees, your transaction fees can be insanely low.

Imagine you have an online store, selling wool hats and you charge $20 per hat.

Paypal charges ~4% commission for validating monetary exchanges of this size. If you make 100 hats, you’re accepting Paypal is going to take 4 of them.

Can you imagine what that represents for merchants around the world?

Companies like Paypal are costing sellers billions and billions of dollars. What if you could reduce your monetary transaction fee to $.01, or even a fraction of a cent?

Blockchain makes this a reality.

Blockchain and Cryptocurrencies allow for Anonymity

Cryptocurrencies built on top of blockchain technology give individuals the capability to carry out transactions anonymously and use money without another party interfering.

Some people like to send value anonymously and some are using blockchain as a tool to get their privacy back.

As the world continues to go digital, governments and big corporations are gaining more control over our personal data.

This includes information as benign as what you studied in college, the name of your first pet, your favorite restaurants but it also includes your spending habits and who you send money to.

The combination of this information makes it easy for nefarious actors to have the tools they need to start controlling your life.

Blockchain products are working to change all that.

Monero, for example, is a cryptocurrency that allows for value exchanges that are impossible to be traced.

There is even a project called Skycoin which seeks to build an anonymous protocol that can compete with the internet.

Giving individuals their freedom back is a trend that will continue within the blockchain arena.

Blockchain and Cryptocurrencies as a Tool Against Against Financial Control

Banks and governments are known to prevent sovereign individuals from spending their own money.

One notable example of a banking failure is the Wikileaks example. Individuals that wanted to donate to Wikileaks (a bold non-profit journalistic organization) in 2010 using traditional banks found their funds frozen.

However, Bitcoin provided an alternative that allowed these same individuals to make donations to Wikileaks without issue.

Freedom as a result of blockchain is more than simply monetary transactions.

When the Chinese government wants to censor internet searches, they can do so with a flip of a switch.

Decentralized exchange systems, such as blockchain, prevents authoritarian regimes from controlling the flow of information.

More examples and closer to home involves your bank account.

As it stands today, the federal government has the ability to freeze and liquidate your assets. Is it really your money if they can leverage this amount of control over you?

This amount of authority over our personal wealth leaves society open to being taken advantage of.

In countries where the government is more corrupted or there exist mafia-like tendencies, money systems based on blockchain are becoming increasingly more valuable.

Blockchain to make Digital Information Unique

Digital currencies are essentially just files, think of MP3’s as an example. Their ability to be replicated, nearly infinitely, makes music hard to commodify.

Blockchain has changed that. Now, we can create digital assets that are unique and unable to be copied. This is all thanks to the distributed-ledger aspect of the technology.

If you were to make a copy of a Bitcoin, you would have to rebuild the entire blockchain!

Is Blockchain Safe?

The main concern people have about blockchains

Hopefully, our blockchain for dummies guide has outlined blockchain technology in a way that shows you how valuable it is.

The largest reasons people point to resisting the adoption of cryptocurrencies is that of safety and security. Specifically, the fear of losing cryptocurrencies to hackers, computer errors, or unforeseen nefarious activity.

Traditional banking is seen as “tried and true.” We’ve been conditioned to use banks and most people have never had significant problems with them. So why would we adopt a new, relatively unproven method of doing the same thing?

Are Blockchains Really Safer Than Traditional Banks?

The reality is that blockchain technology is much safer than traditional banking.

Public blockchains are open-sourced: this allows everyone to inspect the codebase and ensure it works as advertised.

Also, there’s a huge community working to fix any potential issues. Compare this to closed source systems – like banks – where you have to trust them to dictate the rules.

Blockchains operate with three levels of security that protect their users in ways that other alternatives don’t.

- Decentralization

Lacking any single point of failure, digital transactions and other valuable data is safer on the blockchain than any proprietary server. Compare this to a bank which stores its information in centralized servers. - Cryptography

Turning information into a digital code which prevents other users from accessing it. The technology has gotten so robust that even the NSA can’t breach some forms of encryption. Compare your cryptocurrency to fiat currency, can the IRS access your bank account? - Miners and Nodes .

Public blockchains incentivize the verification of transactions. There is not a single party creating trust, it is decentralized across the platform. The distributed nature allows the network to stay operational even in the face of political and environmental disasters.

Trust: Centralized vs Decentralized

The first level of security is decentralization.

If you place your trust in a blockchain rather than a bank, you’re not trusting any single entity. You’re trusting technology.

Transactions are completely automated, there is no human intervention involved with the protocol.

This means there is no centralized authority capable of making huge mistakes or supervising and controlling the actions of participants. As long as the software is running, the system works.

What is Cryptography and Why Does it Improve Security?

The second level of security is cryptography. Or digital signatures to be more specific.

Each and every one transaction is signed by the sender using his private key. Then, the receiver uses the sender’s public key to verify that the transaction was indeed signed by the rightful owner.

Of course, you’ll need to pay careful attention to your private keys, like it’s gold. This will be your responsibility. Keep them secret, keep them safe.

How do Miners/Nodes Work?

The third and final level of blockchain security is miners and/or nodes.

These miners/nodes participate in a blockchain by continually verifying all transactions that occur on that blockchain.

Rewriting or corrupting of a blockchain’s data is virtually impossible because miners/nodes are always ensuring that all of a blockchain’s data stays correct.

In order to change the data in a way that would compromise a blockchain’s integrity, an attacker would have to gain control of the majority of the miners/nodes on a blockchain.

This is called a 51% attack.

Large protocols, like Bitcoin, are safe from this style of attack because of how huge they are.

Many new projects start as an ERC-20 token , which operates on top of the Ethereum protocol. Ethereum is safe and building a new cryptocurrency on top of the Ethereum blockchain is a safe bet.

However, smaller cryptocurrencies building their own blockchain might still face such dangers, and early investors should do their research.

Should you Trust Blockchains?

Decentralization, cryptography, along with miners and nodes, represent three extremely efficient levels of blockchain security.

The technology is always improving and is already far safer than the media makes it sound. You can even gamble on some of the best crypto casinos without worrying that you might get tricked.

People who try to discredit blockchain based on security fears are wrong.

Decentralized blockchain technology is more secure than traditional means of data storage. And so are the decentralized casinos.

The main selling point always reverts back to financial autonomy over assets.

Blockchain puts that power in your hands.

Nowadays there are over 10,000 cryptocurrencies using some form of blockchain technology.

Even the traditional understanding of technology is evolving at a rapid pace.

Each cryptocurrency is different and deserves a thorough level of analysis to understand.

The History of the Blockchain

When did the first work on blockchains begin?

1991 – First work on blockchain-like concept occurred

The first mention of any sort of blockchain-like technology dates back to 1991, when Stuart Haber and W. Scott Stornetta did the first work on a secured chain of blocks .

1992 – Blockchain-like technology improved by incorporating Merkle trees

The next year, 1992, saw the introduction of Merkle Trees to blockchain-like design which enabled multiple documents to be stored in a single block, increasing blockchain efficiency.

When was decentralization first thought of?

2002 – Decentralized trust within a network system was conceptualized

Ten years later, in 2002, the concept of decentralized trust within a network file system was formulated by David Mazieres and Dennis Shasha.

2005 – Bitgold was proposed: A Blockchain-like system with Proof of Work

In 2005, Nick Szabo proposed Bitgold: a protocol for decentralized property titles that incorporated a blockchain-like system.

This protocol involved Proof-of-Work and timestamping features. Unfortunately, BitGold had one fatal weakness.

It was discovered that someone who held a balance of BitGold could spend their coins twice without being “caught” – this weakness became known as the “double-spending problem.”

Bitcoin arrives on the scene!

2008 – Bitcoin’s Whitepaper was published

Everything mentioned up until this point laid the foundation for the first real blockchain.

While Haber, Stornetta, Mazieres, Szabo, etc. were flirting with the concept of a blockchain, a real live blockchain was never actually created until 2008.

In 2008, Satoshi Nakamoto published a paper called Bitcoin – A Peer-to-Peer Electronic Cash System. This paper solved the double-spending problem that troubled Bitgold and would become the white paper written for the first real, working blockchain.

2009 – Bitcoin launched using true blockchain technology

In 2009, with help from programmer Hal Finney and others, Satoshi Nakamoto made Bitcoin a reality.

The code was written, the blockchain was born, and Nakamoto mined the first blocks himself. Hal Finney was the recipient of the very first Bitcoin transaction when he received 10 Bitcoin from Nakamoto.

Blockchains enter mainstream consciousness

2014 – Blockchain innovation gathered attention

The years following Bitcoin’s release saw it gain tremendous popularity and use.

It became seen as a legitimate method of payment – in fact, it was the only one that could be used for certain purposes (like donating to WikiLeaks).

From 2009 to present, we’ve seen huge increases in file sizes on blockchains, innovations that change the way they work, and booms in the prices of cryptocurrencies using blockchain technology.

How have blockchains evolved since Bitcoin?

2014 – Blockchain 2.0: Decentralized Apps and Smart Contracts were conceptualized

In 2014, the term Blockchain 2.0 was first used in The Economist magazine.

Blockchain 2.0 refers to the emergence of applications that can be executed on a blockchain. This innovation represented a massive step forward in blockchain technology.

With this concept, the prospect of running Decentralized Apps (apps that have their code distributed amongst a decentralized network of users rather than stored by a centralized authority) on a blockchain became a possibility and Smart Contracts became plausible, as well.

2015 – Ethereum launched as the first cryptocurrency using Blockchain 2.0

The very next year, 2015, saw the launch of the first Blockchain 2.0. Vitalik Buterin, a contributor during Bitcoin’s creation, saw room for improvement over Bitcoin and wrote the code for Ethereum .

Ethereum promises to provide the same functionality as Bitcoin but will also feature the ability to run Decentralized Apps.

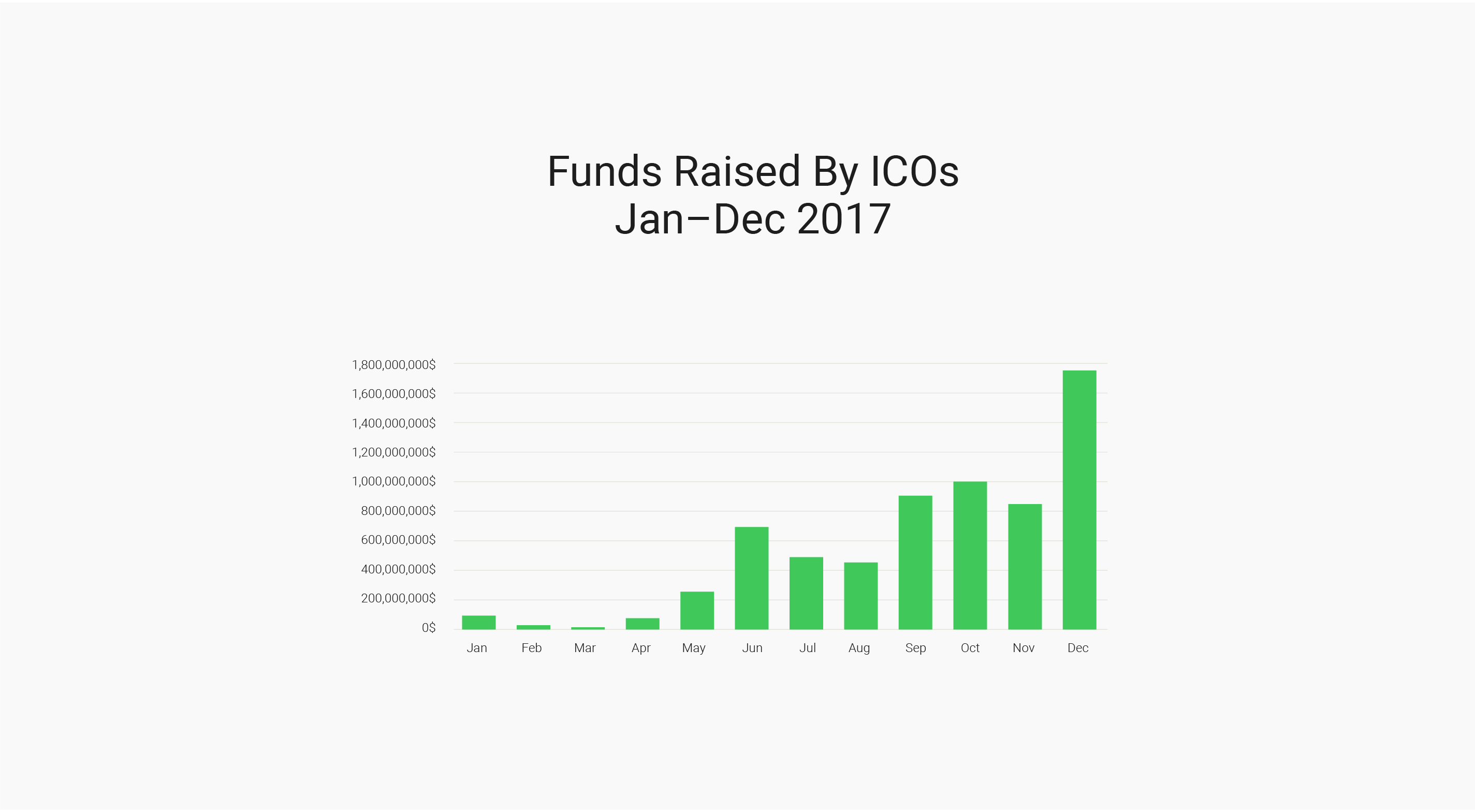

2017 – Initial Coin Offerings and blockchain-based projects became common

While new blockchain-based projects have been appearing since investors and innovators started focusing on blockchain technology in 2014, 2017 was a year marked by an explosion in blockchain-based platforms.

Initial Coin Offerings, also known as ICOs , in which early investors are given the chance to buy the first shares of a project became extremely common in 2017.

Technology Will Continue to Evolve

Blockchain technology is being used and adopted more and more.

From startups to big companies like Google and Amazon, the future is bright. The definition of “blockchain” is changing and not all protocols work exactly the same.

However, the information we provided in this blockchain 101 guide will give you an excellent background for understanding this technology.

As you start to learn about the cryptocurrencies being developed, you’ll discover the nuances that make each coin different.

Congratulations for completing this blockchain 101 guide!

We hope you enjoyed this blockchain 101 guide and learned a lot about blockchain technology.

If you liked our presentation and want to help blockchain’s mass adoption, share our guide with your friends and people with whom you want to see involved.

Our goal at Cryptomaniaks is to be your ultimate guide as you start exploring the wonderful world of cryptocurrencies.

If you want to learn about blockchain technology more in-depth and become an expert, check out the online course of our partner BlockGeeks.

Now that you have a fundamental understanding of the technology behind cryptocurrencies, you can start your cryptocurrency investor journey – if you haven’t yet, as the next guide will focus on how to invest in Bitcoin.

More awesome resources:

- Why Blockchain is more important than ever in 2026?

- Should You Invest in Bitcoin?

- 10 Ways to Make Money with Bitcoin

- The 5 Best Ways to Buy Bitcoin

- 20 Reasons Why Bitcoin Has Value

We're sorry you did not find what you were looking for. Please select the reason this article was not helpful.