Safely Earn Yield on Bitcoin (BTC): Lending, Staking & BTCFi 2026

A concise guide to earning Bitcoin yield in 2025 that compares CeFi lending, BTCFi (Layer‑2/sidechains) and Bitcoin restaking, and prioritizes self‑custody, transparent protocols, and robust risk management.

- Custody over convenience: CeFi yields often require surrendering keys, creating counterparty and insolvency risk that can wipe deposits despite attractive APYs.

- BTCFi and restaking lead: Layer‑2s, sidechains, LSTs and security‑sharing protocols enable non‑custodial, auditable yield and composable DeFi use of BTC.

- Vet and diversify: Favor proof‑of‑reserves, audited contracts, optional insurance, self‑custody options and spread exposure to limit smart‑contract, slashing and liquidity risks.

For over a decade, Bitcoin has been the world’s most trusted store of digital value. But as the ecosystem matures, long-term holders are asking a new question:

Can I safely earn yield on my Bitcoin without giving up custody or taking on unnecessary risk?

In this guide, you’ll learn the key ways to earn yield on Bitcoin in [curren-year], from centralized lending to the growing space of BTCFi and Bitcoin restaking.

We’ll also separate marketing myths from reality, explain where risks lie, and show you how to protect your BTC while generating passive income.

Key takeaways

- CeFi lending is high-risk: Centralized lenders still offer attractive yields but expose users to counterparty and insolvency risk. Lessons from 2022 remain relevant.

- BTCFi is the future: Decentralized Finance on Bitcoin (BTCFi) introduces non-custodial yield through audited smart contracts and Layer 2 innovations like Stacks and Babylon.

- Lending vs. staking: Lending earns interest by letting others use your BTC; “staking” BTC synthetically locks it to secure external chains and earn token rewards.

- Risk management is critical: Always favor platforms with Proof-of-Reserves, audited code, and self-custody options.

Why traditional HODLing isn’t enough: The case for productive Bitcoin

Bitcoin holders, or “HODLers,” are a uniquely patient breed. They believe in BTC’s scarcity, decentralization, and long-term deflationary potential.

But while HODLing has historically outperformed most assets, it comes with a hidden cost: idle capital.

The problem of idle capital

When you hold BTC in cold storage, it’s safe but also static.

Unlike stocks that pay dividends or real estate that generates rent, Bitcoin doesn’t produce yield by itself. As inflation erodes fiat currencies, leaving BTC dormant can mean missing out on additional compounding potential.

The result? A paradox: the world’s most powerful digital asset is often used in the least productive way possible.

BTC HODLer’s dilemma vs. the BTCFI solution

Imagine a teacher who refuses to let students use the internet because “books are enough.” That’s the HODLer’s dilemma, relying only on appreciation while ignoring the growing financial tools that can enhance BTC’s utility.

The modern Bitcoin investor can now earn yield safely through transparent, decentralized systems, without compromising on Bitcoin’s core principle: self-custody.

Let’s explore the three main methods in detail.

DON’T GET REKT

DON’T GET REKT

Curated drops, testnets and red flag alerts straight to your inbox ✌️

Method 1: Centralized Finance (CeFi) lending

CeFi lending was the first way Bitcoin holders earned yield, long before BTCFi or restaking existed. Platforms like BlockFi, Celsius, and Voyager promised “safe” yields between 4–10% APY.

The concept was simple: deposit your BTC, let the platform lend it to institutional traders, and receive a share of the profits.

But as 2022 proved, simplicity can mask serious risks.

How CeFi platforms generate yield on Bitcoin

Centralized lenders act as intermediaries between depositors and borrowers. Your BTC is typically lent to:

- Market makers and hedge funds for liquidity or arbitrage.

- Institutional borrowers seeking leverage to short or hedge BTC positions.

- Other CeFi platforms create a chain of re-hypothecation (your collateral being lent multiple times).

The platform charges borrowers a higher interest rate than it pays depositors, the difference being its profit margin.

On paper, this system seems efficient. In practice, it depends entirely on trust and transparency, and investors’ confidence was shaken badly during the CeFi collapse cycle.

The critical risks of custodial lending

When you deposit BTC on a CeFi platform, you no longer own your coins legally or technically. They become the platform’s assets, and you become an unsecured creditor.

That distinction destroyed billions of dollars in 2022. Celsius, Voyager, and BlockFi, once giants of Bitcoin lending, all filed for bankruptcy, freezing user funds and exposing systemic re-lending risks.

While some survivors (like Nexo or Ledn) have improved transparency through Proof-of-Reserves audits, the fundamental issue remains:

CeFi yield requires you to trust a middleman.

For many Bitcoin users, that violates the entire ethos of decentralized finance.

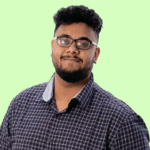

Method 2: Bitcoin decentralized finance (BTCFi)

The next evolution of earning yield on Bitcoin is happening not on centralized platforms, but within the Bitcoin ecosystem itself.

BTCFi, short for Bitcoin Decentralized Finance, is the term for protocols that bring DeFi-style tools (lending, liquidity pools, staking) to Bitcoin holders without requiring centralized custody.

Understanding BTCFi’s core mechanics

Bitcoin’s Layer 1 blockchain is highly secure but intentionally limited: it doesn’t support smart contracts. BTCFi solves this by moving functionality to secondary layers or sidechains, such as:

- Stacks (STX): A Layer 2 smart contract platform secured by Bitcoin via its Proof-of-Transfer consensus.

- RSK (Rootstock): An Ethereum-compatible sidechain pegged to Bitcoin, enabling lending and yield farming.

- Babylon: A security-sharing protocol that allows Bitcoin to secure Proof-of-Stake (PoS) chains.

Additionally, BTCFi often involves tokenized versions of BTC like Wrapped Bitcoin (wBTC) or sBTC, allowing BTC to be used in DeFi protocols such as Aave, Compound, or Balancer on Ethereum and its L2 networks.

These tokens are typically backed 1:1 by Bitcoin held in custody. Though again, verifying that backing is critical.

Yield generation via decentralized lending Pools

In BTCFi, you can deposit wrapped BTC into decentralized lending protocols or liquidity pools. Here’s how yield is generated:

- Lending Pools: Lend BTC to borrowers via smart contracts and earn variable interest rates based on supply/demand.

- Liquidity Provision (LPing): Provide BTC pairs (e.g., BTC/ETH or BTC/USDC) to decentralized exchanges, earning trading fees and reward tokens.

However, BTCFi is not risk-free. The biggest dangers are smart contract vulnerabilities and impermanent loss, which occurs when the price of your deposited assets diverges and reduces your LP value.

Yet, compared to CeFi, BTCFi’s transparency is a major upgrade. All transactions are on-chain, and smart contract audits can be independently verified.

As 2025 progresses, BTCFi is expected to become a cornerstone of Bitcoin’s second-layer economy, balancing yield potential with user sovereignty.

Method 3: The true nature of “Bitcoin staking” and liquid restaking

The phrase “Bitcoin staking” can be misleading. Bitcoin runs on Proof-of-Work (PoW); there’s nothing to “stake” in the native network. So when platforms advertise Bitcoin staking, they usually mean one of two things:

- Lending disguised as staking (i.e., custodial interest accounts), or

- Synthetic staking, where BTC is locked to secure an external PoS chain.

Let’s unpack how the latter works, because it’s one of the most promising frontiers in BTC yield.

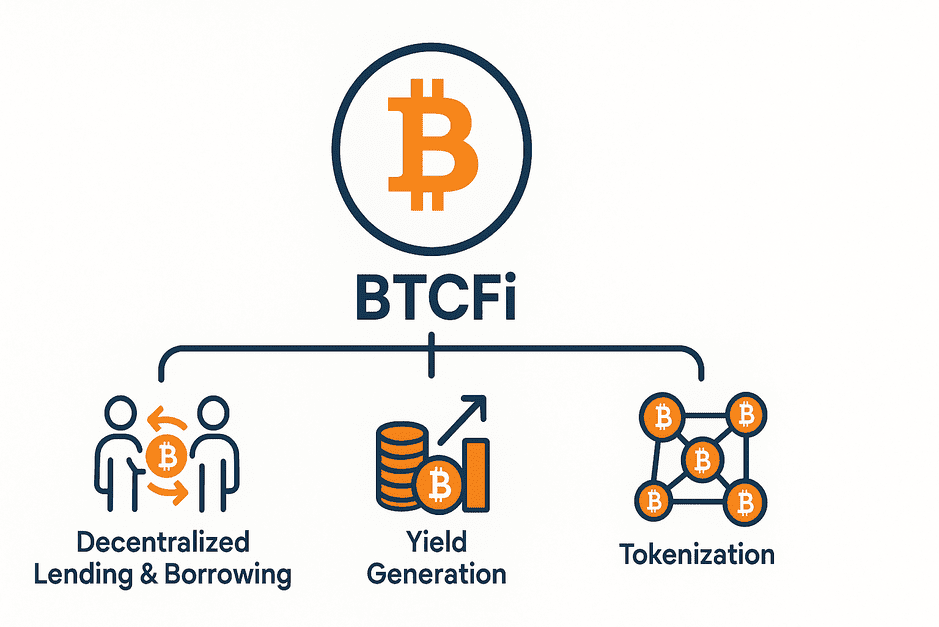

Bitcoin’s PoW vs. synthetic staking protocols (Babylon)

New protocols like Babylon are pioneering a model called Bitcoin security sharing. Instead of altering Bitcoin’s base layer, they allow BTC holders to lock their coins in time-locked smart contracts that function as vaults. The locked BTC are then used to secure other PoS networks by providing collateral that can be “slashed” if malicious activity occurs.

In exchange, stakers earn yield in the form of the external network’s native tokens.

This approach effectively transforms Bitcoin’s static value into an economic security layer for other chains, while maintaining Bitcoin’s immutability. It can be used as a passive income strategy by BTC holders.

Babylon’s concept of time-locked BTC security could redefine Bitcoin’s role in multi-chain ecosystems, creating a bridge between BTC’s safety and the yield potential of PoS systems.

Comparing liquid staking tokens (LSTs) for BTC

To make staking more flexible, developers are introducing Liquid Staking Tokens (LSTs). These are tokenized receipts representing locked BTC that can still be used in DeFi.

Imagine locking 1 BTC into a Babylon vault and receiving bBTC in return. You can then trade, lend, or restake bBTC elsewhere, compounding your yield opportunities.

This concept, known as BTC restaking, mirrors what Ethereum users do with LSTs like stETH and rsETH, effectively allowing BTC holders to participate in complex, yield-layered ecosystems.

While this technology is still early in development, it’s shaping up to be the most secure and capital-efficient form of Bitcoin yield, one that could outlive speculative lending entirely.

Unbiased risk assessment: Chasing APY is a risky bet

Let’s be blunt: the higher the advertised APY, the higher the hidden risk. Earning yield on Bitcoin isn’t always about chasing the biggest number, but about preserving your principal while allowing modest compounding over time.

The risk-return spectrum for BTC yield

| Method | Typical APY | Key Risks | Custody Type |

CeFi Lending |

3–8% | Counterparty risk, insolvency, re-hypothecation | Custodial |

BTCFi Lending / LPing |

2–6% | Smart contract bugs, impermanent loss, liquidity risk | Non-custodial |

BTC Staking / Restaking |

4–10% | Protocol failure, slashing risk, LST depegging | Non-custodial / hybrid |

Smart contracts can fail, and even decentralized systems can face liquidity crunches or exploit attempts. Diversification remains your best defense across methods, platforms, and custody types. All potential yield rates are based on historical data.

Vetting a platform: The CryptoManiaks trust checklist

Before committing any BTC to a yield platform, apply this four-step due diligence process:

- Proof-of-reserves & transparency: The platform must publish on-chain or third-party verified reserves.

- Audited smart contracts: Only interact with protocols that have undergone independent security audits (Eg: CertiK or Halborn).

- Insurance or guarantee policies: Look for optional coverage (e.g., Nexus Mutual, InsurAce) against contract failure, but treat it as supplementary, not primary protection.

- Self-custody options: Prefer solutions where you control the private keys (native BTCFi or restaking protocols). If a platform can freeze your withdrawals, it’s not truly decentralized.

Conclusion: Custody over convenience, always

The scope for earning Bitcoin yield in 2026 is richer and riskier than ever, but the principle remains unchanged: not your keys, not your coins.

CeFi platforms may tempt you with high, stable APYs, but those numbers often mask opaque practices and systemic risk. BTCFi protocols, while newer, offer transparent, auditable, and non-custodial alternatives that align better with Bitcoin’s ethos.

Before you stake or lend:

- Make sure you understand Slashing, Impermanent Loss, and Counterparty Risk.

- Avoid projects with vague tokenomics or unsustainable reward emissions.

- Keep the majority of your BTC in cold storage or non-custodial systems.

Bitcoin was built to eliminate intermediaries, not depend on them. In that spirit, let your BTC work for you, not for someone else.

If 2022 was the year of reckless yield chasing, 2026 is the year of responsible BTC productivity. With BTCFi and restaking maturing rapidly, you no longer have to choose between safety and utility.

Earn yield, but do it the Bitcoin way: transparently, self-sovereignly, and with full awareness of your risk.

Neither CeFi nor DeFi platforms are covered by FDIC or government insurance. Some projects offer private insurance pools, but they are limited in scope and coverage. Always treat BTC yield platforms as investment tools, not savings accounts.

While yields are still modest, these protocols offer the best balance of self-custody and productivity, providing a glimpse at Bitcoin’s financial future.

We're sorry you did not find what you were looking for. Please select the reason this article was not helpful.