How to Earn USDT Passive Income Safely: CeFi vs DeFi Strategies

AI Overview

AI Overview

What’s This?

An artificial intelligence tool created this summary, which was based on the text of the article and checked by an editor. Read more about how we use artificial intelligence in our journalism.Practical guide to earning passive income with USDT in 2025, comparing CeFi and DeFi yields (roughly 4–15%) and trade-offs, and recommending balanced allocations that prioritize transparent, sustainable sources of yield.

- Main trade-off: CeFi = ease and custodial risk with ~4–10% APY; DeFi = higher potential (6–15%) but smart‑contract and peg risks.

- Practical strategy: Hold a CeFi savings base for steady yield, add reputable DeFi lending or stable-stable LPs, and allocate a small portion to auto-compounding vaults.

- Risk controls: Diversify across platforms, prefer blue‑chip protocols, enable 2FA/hardware wallets, consider insurance, and verify where yields come from.

After several positive regulatory developments like the GENIUS Act, USD-pegged stablecoins have become a popular financing tool for investors across the board.

Stablecoins like Tether (USDT) have become popular for traders who want to hold digital dollars and still earn a return.

Unlike volatile tokens, USDT is pegged to the US dollar, making it attractive for generating passive income.

In 2025, both centralized finance (CeFi) and decentralized finance (DeFi) offer ways to put USDT to work. The strategies vary in complexity, potential yield, and risk.

This guide explains how USDT holders can approach passive income, what returns to expect, and how to compare Tether yield strategies.

USDT Yield: CeFi vs DeFi

- CeFi (centralized finance): Platforms or exchanges manage your USDT and pay you interest. Easy to use, moderate potential yield, but requires trust in the company.

- DeFi (decentralized finance): You deposit USDT into smart contracts. DeFi offers more control and potentially higher returns, but it is prone to hacks and can be complex for beginner users.

CeFi strategies for USDT passive income

Savings accounts and earn programs (risk: moderate)

Most large exchanges and fintech platforms offer USDT savings accounts where you deposit and earn interest. The platform lends your USDT to borrowers or traders and pays you a share.

- How it works: Deposit USDT → earn daily or weekly interest → withdraw anytime.

- Potential yield: Around 4–8% APY depending on market demand.

- Risk: Custodial risk. If the platform fails, withdrawals could be delayed or blocked.

This option is the simplest and most beginner-friendly. It feels similar to a traditional bank savings account but with higher potential returns.

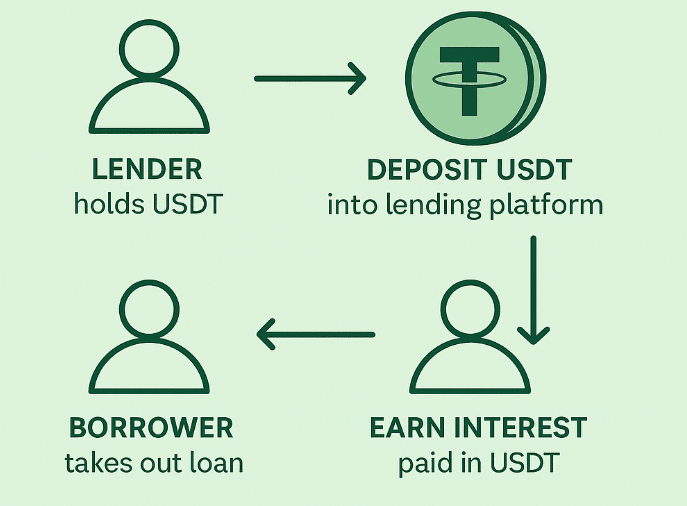

Centralized lending platforms (risk: moderate)

Some CeFi lenders specialize in offering yield on stablecoins. You deposit USDT, and they lend it out to overcollateralized borrowers.

- How it works: Deposit USDT into a lending program → earn interest paid in USDT.

- Potential yield: 6–12% APY, depending on borrower demand.

- Risk: Relies on the lender’s solvency and loan management practices.

Although yields can be attractive, users should avoid chasing unusually high advertised rates, as these often involve additional risks.

Margin lending on exchanges (risk: moderate)

Exchanges with margin trading offer P2P lending markets. Here, you lend your USDT directly to traders who need leverage.

- How it works: Place your USDT into the margin funding pool → earn interest from traders borrowing it.

- Potential yield: 5–10% APY, but rates fluctuate based on trading demand.

- Risk: Depends on the exchange’s risk management system. If liquidation systems fail, lenders could be affected.

This option can be semi-passive. Some exchanges allow auto-lending at the market rate so you don’t have to adjust settings manually.

DeFi strategies for USDT passive income

Lending protocols (risk: moderate)

Protocols like Aave, Compound, and Solend let you supply USDT into lending pools. Borrowers post more collateral than they borrow, and lenders earn the interest.

- How it works: Deposit USDT → receive interest-bearing tokens → withdraw with interest.

- Potential yield: 4–8% APY on large networks like Ethereum; sometimes 8–12% APY on Solana, Avalanche, or BNB Chain when demand spikes.

- Risk: Smart contract bugs or stablecoin depeg. Established protocols reduce this risk but cannot eliminate it completely.

This is one of the most straightforward and widely used stablecoin lending strategies.

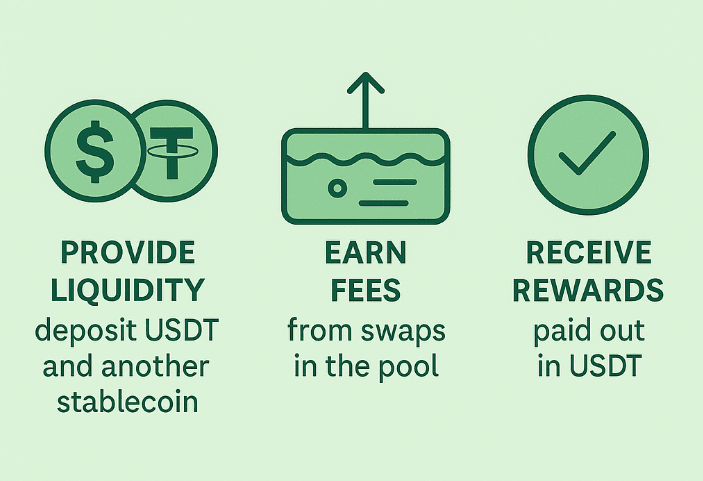

Stablecoin liquidity pools (risk: moderate)

You can provide liquidity to decentralized exchanges (DEXs) in pools pairing USDT with another stablecoin (e.g., USDC or DAI). These pools earn trading fees and token incentives.

- How it works: Deposit USDT + another stablecoin into a pool → earn trading fees and reward tokens.

- Potential yield: 6–12% APY depending on trading volume and rewards.

- Risk: Smart contract exploits or one stablecoin losing its peg.

Because both sides of the pool are stable, the price risk is lower than with crypto-crypto pools, making this a conservative way to farm yield.

Yield farming with auto-compounding (risk: moderate to high)

Yield aggregators like Yearn or Beefy Finance optimize returns by auto-compounding rewards. They take the tokens you earn and reinvest them for a higher effective yield.

- How it works: Deposit USDT or USDT LP tokens → aggregator auto-compounds rewards → balance grows over time.

- Potential yield: 8–15% APY, sometimes higher with incentives.

- Risk: Extra smart contract layer, plus reliance on reward token prices.

This strategy requires some familiarity with DeFi, but is still manageable for beginners willing to learn.

Real-world asset (RWA) strategies (risk: low to moderate)

Some protocols invest stablecoins into tokenized US Treasuries or bonds. While not strictly “USDT” strategies, you can swap into these easily.

- How it works: Deposit USDT into a protocol → it converts into yield-bearing tokens backed by real assets.

- Potential yield: 5–8% APY, closely aligned with Treasury yields.

- Risk: Smart contract risk plus regulatory risk, but generally lower than experimental DeFi.

This is becoming popular as a safer base layer of Tether yield, similar to a money market fund.

USDT yield strategy comparison

Strategy |

How it works | Potential yield (APY) | Risk level | Suitable for beginners? |

| CeFi savings account | Deposit USDT into platform account | 4–8% | Moderate | Yes |

| CeFi lending | Lender manages loans to borrowers | 6–12% | Moderate | Yes |

| Margin lending | Fund traders directly on exchange | 5–10% | Moderate | Somewhat |

| DeFi lending | Supply USDT to lending pool | 4–10% | Moderate | Yes |

| Stablecoin liquidity pools | Provide USDT + another stablecoin | 6–12% | Moderate | Yes |

| Yield farming vaults | Auto-compounding stablecoin farms | 8–15% | Moderate–High | With caution |

| RWA strategies | Convert into tokenized Treasuries | 5–8% | Low–Moderate | Yes |

Key trends in 2025

- More realistic yields: Sustainable APYs on USDT now range potentially between 4–12%. Anything much higher usually involves higher risk or short-term incentives.

- Closer link to traditional finance: US interest rates around 5% influence baseline stablecoin yields. Many protocols now anchor to real-world returns.

- Better risk tools: Insurance products, proof-of-reserves, and dashboards give clearer insight into platform safety.

- Hybrid CeDeFi platforms: Some providers combine CeFi simplicity with DeFi yield sources, offering self-custody and automated strategies.

Final thoughts

Earning USDT passive income in 2025 is much safer and more transparent than in the early days of DeFi. CeFi offers simplicity and steady but moderate returns. DeFi gives more control and sometimes higher potential yield through stablecoin lending and farming, but requires care regarding smart contract risks.

For beginners, a balanced approach works best:

- Keep some USDT in a CeFi savings account for a stable passive income.

- Use a reputable DeFi lending pool for additional passive income.

- Experiment with a small portion in liquidity pools or auto-compounding vaults if comfortable.

The most important step is always to ask, “Where does this yield come from?” If the answer is clear and sustainable, the strategy is likely worth considering. If it seems vague or unusually high, treat it with caution.

-

01.

What is the safest way to earn USDT passive income in 2025?

For most beginners, start with a CeFi savings account on a reputable exchange or a blue-chip DeFi lending pool (e.g., Aave-style markets). These are simple, transparent, and potentially offer 4–8% APY in normal conditions. Keep funds diversified, enable 2FA, and avoid platforms that cannot explain where yield comes from. Consider optional DeFi insurance on major protocols for extra protection.

-

02.

CeFi vs DeFi: which pays higher Tether yield, and what are the risks?

DeFi can potentially pay more (often 6–12% APY via lending or stablecoin LPs, and up to the low-teens with auto-compounding). You keep self-custody but face smart contract risk and variable rewards. CeFi is easier to use and potentially pays 4–10% APY, but you accept platform (custodial) risk. Many users blend both: a CeFi base for simplicity, plus a DeFi position for higher potential yield.

-

03.

How can I reduce risk while earning USDT passive income?

Use a three-step plan:

- Diversify across CeFi and DeFi so that no single failure harms your whole balance.

- Stick to stablecoin lending and stable-stable LPs on established protocols; avoid chasing very high APYs without clear sources.

- Add safeguards: use hardware wallets, monitor APY/peg health, and consider DeFi insurance on core positions. Reassess monthly and rebalance if yields or risks change.

We're sorry you did not find what you were looking for. Please select the reason this article was not helpful.